Image

Reprinted with permission from Pew Charitable Trusts. Image Marianna Armata Flickr

State governments face increased costs and potential budget challenges linked to historically high inflation rates. From price spikes for construction materials to labor, the rising costs of goods and services are disrupting state finances on both sides of the ledger.

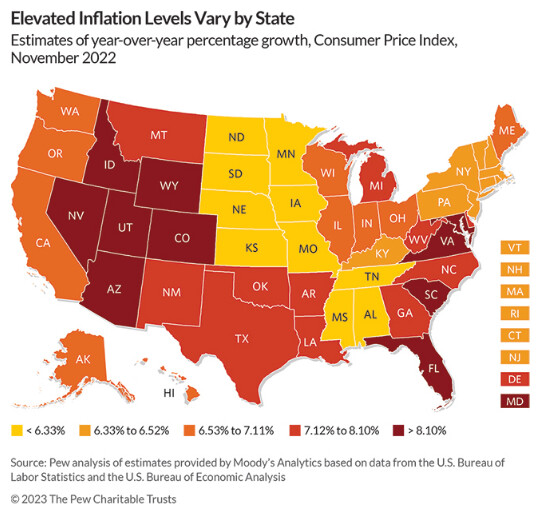

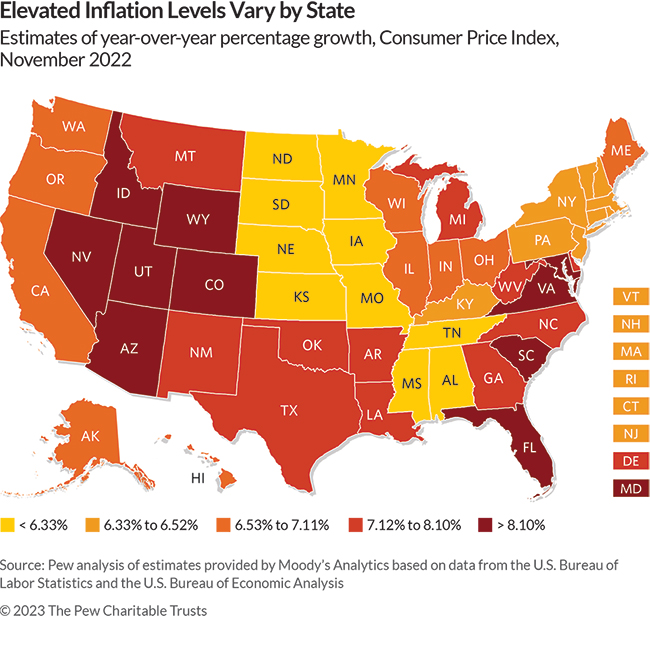

Every state has experienced higher costs, but prices in some states have risen more than in others. Nationally, the consumer price index rose 7.1% in November 2022 over the past year—a slower increase than in recent months, yet still more than three times the norm of the past three decades. For November, increases ranged from a high of more than 8.3% in Colorado, Florida, Nevada, and Utah to a low of less than 6.1% in Minnesota, North Dakota, and South Dakota.

Despite some limited relief recently, rising costs are driving up spending on payroll, infrastructure, and other major areas of state budgets. They also are disrupting tax revenue trends through slowing consumer demand, rising wages, and increased stock market volatility.

Inflation’s rapid escalation to historic highs may have started to ease in the short term. Still, it has proved more persistent than the Federal Reserve initially forecasted and is not expected to return to normal levels for some time. Fortunately, record levels of rainy day funds and significant amounts of flexible federal aid will provide states with extra breathing room to help manage budget uncertainties in the short term. Persistently high inflation, however, would exacerbate many of the long-term fiscal risks that states already face.

Inflation affects tax collections, but exactly how much depends on the extent that each state relies on specific tax types and how each revenue stream is structured. Nationally, two-thirds of total tax dollars come from levies on personal income and general sales of goods and services, but the mix varies widely. Five states don’t collect general sales taxes, for example, and nine don’t collect broad-based personal income taxes.

Sales taxes are generally calculated as a percentage of nominal prices, so collections closely track the ups and downs of inflation. States also levy sales taxes differently from one another, which influences how inflation can drive changes in collections in some states more than others. For example, most states tax the purchase of goods, while fewer collect taxes on a broad range of services. Differences in price spikes among goods and services then influence overall sales tax collections.

Although a temporary spike in inflation can boost sales tax revenue, persistently high inflation has historically led to decreased consumer and business spending and, as a result, weaker collections. Should persistent inflation and actions aimed at taming it trigger a recession, spending and related sales tax revenue would decline even further.

Personal income taxes are collected on many types of income, and how much each state relies on individual sources influences how rising costs affect overall collections. For example, state taxes on wages and salaries make up the lion’s share and tend to grow faster during periods of elevated inflation as employers look to increase worker pay to help compensate for the rising costs of living. Taxes collected on capital gains are another common income source and particularly important to some states, including California and New York. These payments tend to become more volatile as asset prices fluctuate in response to the effects of elevated inflation and rising interest rates.

Increased tax liability from income growth can also result in individuals and households being pushed into higher state income tax brackets—which results in more tax collections. This phenomenon, sometimes called “bracket creep,” can be particularly acute during times of high inflation within the 15 states that do not adjust their individual tax brackets for inflation, according to the Tax Foundation.

Elevated inflation is driving up state government costs across a wide range of expenditures: from goods to payroll and contracts with service providers. Annual state expenditures grew by an estimated 18.3% by the end of fiscal year 2022 compared with a year earlier, the highest annual increase in at least 44 years. A variety of factors, including rising inflation, fueled the growth, according to the National Association of State Budget Officers.

Rapid inflation adds pressure for states to spend more on payroll—which accounts for roughly one-fifth of their operating costs—to retain state workers and attract new ones. This demand is amplified by a historic gap between government and private sector pay growth. State employee wage growth above budget assumptions can also create new unfunded long-term liabilities within state pension systems that can, in turn, increase required annual pension contributions.

Declining purchasing power due to rising prices reduces the capacity of state appropriations to accomplish policy priorities, such as infrastructure projects. Rapidly increasing construction costs are forcing some states to delay infrastructure projects, scale projects back, or spend significantly more than anticipated. This can be a particular challenge for states with urgent needs to replace or repair critical infrastructure.

A fiscal outlook released by the California Legislative Analyst’s Office (LAO) in November indicated that the state could face sizable budget deficits in each year from fiscal year 2023-24 through fiscal 2026-27. And because the outlook reflected only inflationary adjustments for certain spending areas—in accordance with California law and policy—the LAO cautioned that the true cost to maintain existing service levels would be greater than what is shown in its analysis.

In a related brief, the office discussed the consequences—such as declines in the quantity and quality of services—of excluding inflationary adjustments from budgeted spending. The brief encouraged policymakers to take inflation into consideration when addressing the anticipated budget deficit. For instance, pausing automatic inflationary adjustments could help free up state funds, while implementing new adjustments for inflation in certain areas to offset increased prices would exacerbate a deficit.

Another risk related to inflation is that the Federal Reserve’s actions to tame high prices could trigger an economic downturn, which would open up budget deficits. States can incorporate this possibility into their forecasts to better prepare.

In Oregon, for example, alternative economic scenarios are routinely included in the quarterly economic and revenue forecasts produced by the state’s Office of Economic Analysis (OEA). The OEA typically projects revenue under two alternative economic scenarios, based on either optimistic or pessimistic assumptions relative to the baseline forecast. However, in the forecasts released from December 2021 through September 2022, the optimistic and pessimistic scenarios were replaced by a “boom/bust scenario” in which Federal Reserve actions trigger a recession due to “the current economic dynamics and potential for inflation to run hotter, for longer.”

The boom/bust scenario included in the September forecast assumed that the Federal Reserve would raise interest rates because inflation would prove more persistent than expected—and a “relatively mild” brief recession would ensue. The OEA’s projections showed that under this scenario, general fund revenue was expected to come in as much as $1.34 billion below the baseline forecast.

Having this type of data readily available can help policymakers make informed budget decisions as they continue to grapple with elevated inflation and its many unknowns.

Sheanna Gomes is an associate manager and Justin Theal is an officer with The Pew Charitable Trusts’ state fiscal policy project.

Partly Cloudy , with a high of 32 and low of 17 degrees. Overcast for the morning, partly cloudy for the afternoon, clear in the evening,